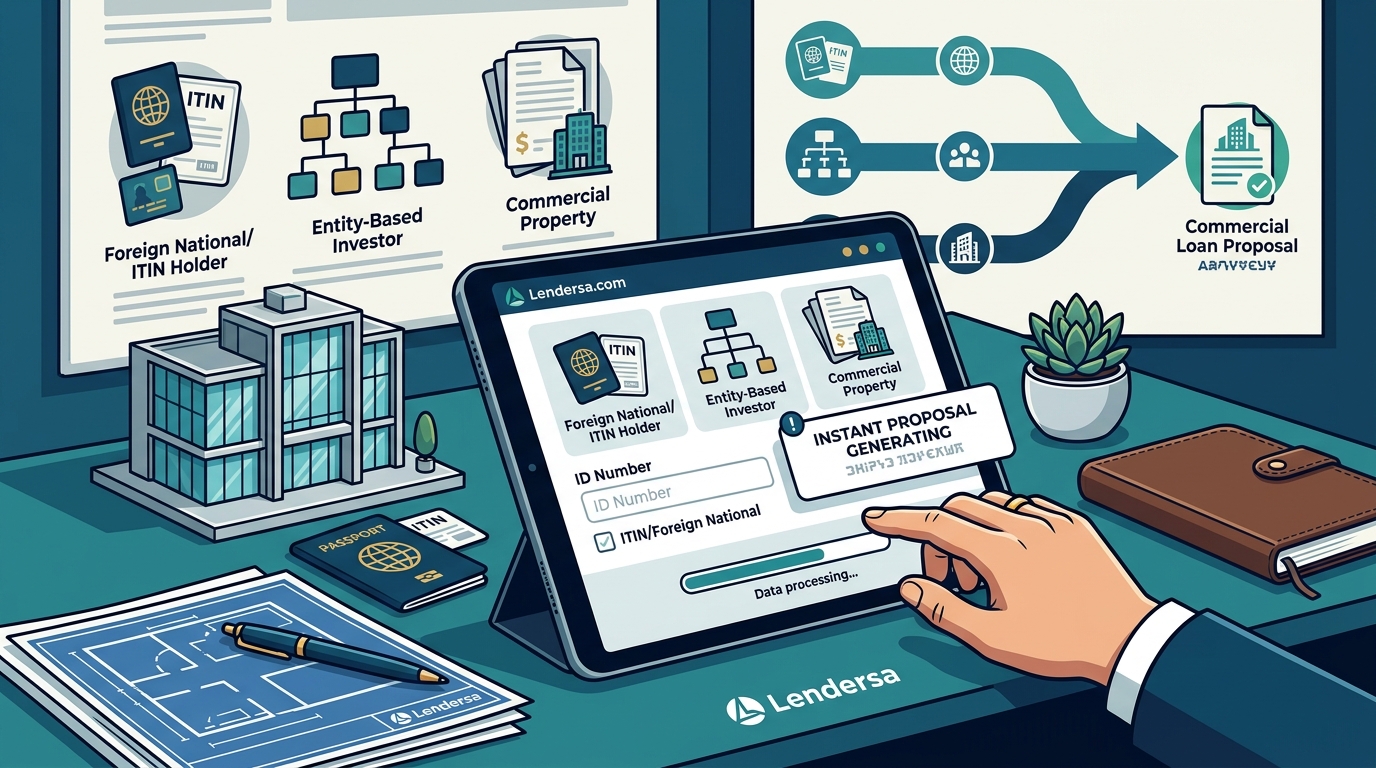

Thousands of foreign nationals, ITIN holders, and entity-based investors close on U.S. commercial real estate every year without ever entering a Social Security Number. This tutorial shows you three distinct paths to an instant loan proposal and helps you pick the one that matches your situation—then walks you through the exact workflow on Lendersa.com.

Why Commercial Lenders Can Work Without an SSN

Traditional residential mortgages almost always demand an SSN because the loan is sold to agencies like Fannie Mae. Commercial deals are different. Many lenders hold commercial loans on their own balance sheets or package them as CMBS, and they have wide latitude in how they verify a borrower.

Non-QM lending, the umbrella category that covers these products, has grown rapidly. Non-QM originations topped $120 billion in 2025 and could reach $150–$180 billion in 2026. At the same time, foreign-national loan programs explicitly require no U.S. tax returns, SSN, or domestic credit history. Lenders that serve this segment verify identity through passports, ITINs, or entity documentation and evaluate risk primarily through the property’s income performance or appraised value.

Federal regulations such as the USA PATRIOT Act require identity verification, but they do not mandate that the identifier must be an SSN. Lenders satisfy these obligations through alternative means like an ITIN, a passport, or a valid visa combined with entity-level documentation.

Decision Tree: Which Financing Path Fits You?

| Your Situation | Recommended Path | Typical Speed to Proposal |

|---|---|---|

| You hold an IRS-issued ITIN and have filed U.S. taxes | Path A – ITIN Loan | Minutes (via Lendersa AI matching) |

| You are a foreign national with a passport but no U.S. tax ID | Path B – Foreign National Program | Minutes to hours |

| You invest through an LLC or corporation and want entity-only underwriting | Path C – DSCR / Entity-Based | Minutes (via Lendersa AI matching) |

Path A – ITIN-Based Commercial Loan Proposal

Who This Is For

Entrepreneurs, self-employed individuals, and immigrant investors who hold a valid Individual Taxpayer Identification Number. ITIN loans are classified as non-QM because they do not meet the lending criteria set by Fannie Mae and Freddie Mac. They are usually held in lender portfolios or sold to private investors.

What to Gather Before You Click

- Valid ITIN letter (CP565 notice) – ITINs that have not been used on a federal tax return for three consecutive years expire and must be renewed via IRS Form W-7.

- Government-issued photo ID from country of origin (passport or consular ID).

- Property details – address, property type (office, retail, multifamily 5+, mixed-use, warehouse), estimated value, and intended use.

- Income documentation – two years of U.S. tax returns, 12–24 months of bank statements, or a CPA-prepared profit-and-loss statement.

- Down payment evidence – ITIN commercial programs typically require 10% to 20% down.

How the Proposal Arrives

- Enter property details and loan amount on Lendersa.com. No SSN field is required to start.

- The AI engine matches your scenario against hundreds of lending programs, including ITIN-friendly non-QM lenders.

- Multiple lenders compete to present you with a term sheet showing rate, LTV, estimated closing costs, and required documentation.

- You pick the best proposal and begin formal underwriting.

Path B – Foreign National / Passport-Only Proposal

Who This Is For

International investors who live primarily outside the United States and do not have a U.S. tax ID of any kind. Some lenders and fintech companies verify identity using a passport, visa, or other government-issued ID rather than an SSN.

What to Gather

- Valid passport (plus visa if applicable).

- Property address, type, and purchase price or refinance value.

- Proof of funds for down payment (foreign bank statements accepted by many lenders).

- Entity formation documents if purchasing through a U.S. LLC (recommended for liability protection).

What Lenders Evaluate Instead of a Credit Score

Without a U.S. credit file, lenders lean on the deal itself. For income-producing commercial properties, a Debt Service Coverage Ratio (DSCR) of 1.0 or higher—meaning the property’s monthly rent covers the monthly mortgage payment—is often the primary qualifier. The median DSCR that commercial lenders require is around 1.25. Many programs also have no minimum credit score requirements on commercial programs and use strictly collateral-based lending.

Path C – Entity-Only DSCR Proposal (No Personal ID at Intake)

Who This Is For

U.S.-based or international investors who purchase through an LLC or corporation and want the initial proposal generated purely on entity and property data. The borrower’s personal financials are not part of the initial quote.

What to Gather

- LLC or corporate formation documents (Articles of Organization, EIN confirmation).

- Property address, type, current or projected rental income, and estimated market value.

- Loan amount and purpose (purchase, refinance, cash-out).

How DSCR Underwriting Works

DSCR loans qualify based on the rental income of the investment property. No personal income verification is needed. The formula is simple: DSCR = Monthly Rent ÷ Monthly Mortgage Payment. A ratio of 1.0 or above typically qualifies. LLC ownership is allowed, and many programs have no limit on the number of financed properties.

On Lendersa, you enter entity details and property financials. The platform’s AI returns competing DSCR proposals from multiple lenders—often within minutes—so you can compare rates, leverage, and fees side by side.

Putting It Together: The Lendersa Workflow

Lendersa is a loan marketplace where lenders compete for your deal. Here is the workflow that applies to all three paths above.

- Visit Lendersa.com and select your property type. Options include residential (1–4 units), commercial (5+ units, office, retail, industrial, mixed-use), and vacant land.

- Enter property and financial details. The form asks for property value, loan amount, property location, and intended use. It does not require an SSN to generate proposals.

- AI matching runs instantly. Lendersa’s engine evaluates your scenario against both conventional and hard money lending programs to surface the most competitive options.

- Review competing proposals. Each proposal includes the lender’s rate, estimated LTV, term length, prepayment penalty structure, and closing timeline.

- Select a lender and proceed. You connect directly with the lender to supply formal documentation (ITIN letter, passport, entity docs, or bank statements depending on your path).

Three Real-World Scenarios

Scenario 1: Strip Mall Purchase With an ITIN

A self-employed business owner in Houston holds an ITIN and has filed U.S. taxes for four years. She wants to buy a $950,000 strip mall generating $8,200 per month in rent. She enters the deal into Lendersa, selects “commercial,” and receives three proposals within minutes: a 75% LTV hard money bridge at 10.5%, a non-QM DSCR loan at 8.9% requiring 25% down, and a portfolio lender offering 7.8% with full documentation. She chooses the portfolio lender, uploads her ITIN letter, two years of returns, and bank statements, and moves to underwriting.

Scenario 2: Foreign Investor Buying a Warehouse

A Canadian investor with no U.S. tax history wants to purchase a $1.4 million warehouse in Phoenix. He forms a Wyoming LLC, enters the deal on Lendersa, and receives two foreign-national program proposals. Both evaluate the property’s DSCR (projected rent of $11,000/month versus an estimated mortgage payment of $8,600/month = 1.28 DSCR). The winning proposal offers 65% LTV with a 12-month bridge term and a clear path to permanent DSCR financing.

Scenario 3: Domestic LLC Buying a Mixed-Use Building

Two U.S.-based partners own an LLC with an EIN but prefer not to supply personal SSNs at the proposal stage. They enter their mixed-use property details—$2.1 million purchase, $14,500/month in rent—into Lendersa. The AI returns four DSCR proposals. They pick a 30-year fixed at 7.6% with no personal income verification and 25% down, then provide entity documents and a personal guarantee only at the formal application stage.

Common Pitfalls That Delay Your Proposal

- Expired ITIN. An ITIN not used on a tax return for three years lapses. Renew it before applying.

- Missing entity documents. If you invest through an LLC, have your EIN confirmation letter and operating agreement ready.

- Inaccurate rent projections. Lenders verify rental income against market data. Overstating rent will stall underwriting.

- Skipping the comparison step. Non-QM rates vary significantly between lenders. Rates can run 0.50% to 1.50% above conventional, so comparing multiple proposals is essential.

- Confusing a proposal with a commitment. An instant proposal is a preliminary term sheet. Full approval comes after underwriting reviews your documentation.

Key Takeaways

- You do not need an SSN to receive an instant commercial loan proposal. Three viable paths exist: ITIN, foreign national, and entity-based DSCR.

- Non-QM commercial lending is a mature, regulated market projected to exceed $150 billion in originations in 2026.

- DSCR loans evaluate the property’s income, not yours. A ratio of 1.0 or higher typically qualifies.

- Lendersa’s AI marketplace lets multiple lenders compete on your deal, and no SSN is required to start.

- Prepare your alternative ID (ITIN letter or passport), entity documents, and property financials before you submit to get the fastest proposals.

Frequently Asked Questions

Can I really get a commercial loan proposal without providing my Social Security Number?

Yes. Many commercial lenders use non-QM and hard money programs that verify identity through ITINs, passports, or entity documentation instead of an SSN. Platforms like Lendersa do not require an SSN to generate initial proposals. The SSN may be requested later during formal underwriting by some lenders, but many DSCR and foreign-national programs never require one.

What is an ITIN and how does it replace an SSN for lending purposes?

An Individual Taxpayer Identification Number (ITIN) is a tax processing number issued by the IRS to individuals who are not eligible for an SSN but need to file U.S. tax returns. ITIN loans are non-QM mortgage products that accept this number in place of an SSN for identity verification and credit evaluation. They typically require 10% to 20% down and may accept alternative credit history such as rent and utility payments.

What types of commercial properties qualify for no-SSN loan proposals?

Most asset-based and DSCR lenders finance office buildings, retail properties, mixed-use buildings, industrial warehouses, and multifamily complexes with five or more units. Lendersa also supports vacant land. Eligible property types may vary by lender, so submitting your deal to a marketplace that surfaces multiple options is the most efficient approach.

How quickly can I receive a loan proposal on Lendersa?

Lendersa uses AI to match your scenario against conventional and hard money lending programs in seconds. Most users see competing proposals within minutes of submitting their property and financial details. Formal approval timelines depend on the lender and the documentation path you follow.

Are interest rates higher for commercial loans without an SSN?

Non-QM and foreign-national commercial loans typically carry rates 0.50% to 1.50% above conventional financing. However, rates vary widely by lender, which is why comparing proposals on a marketplace like Lendersa is critical. A strong DSCR, a larger down payment, or substantial liquid reserves can help you secure more competitive terms.

Do I need a U.S. bank account to get a commercial loan proposal?

Not for the initial proposal. However, most lenders will require a U.S. bank account before closing. Foreign nationals can often open a U.S. account with a passport and ITIN or EIN. Forming a U.S. LLC and obtaining an EIN simplifies this process.