How to Compare Hard Money Loan Rates Without a Credit Pull

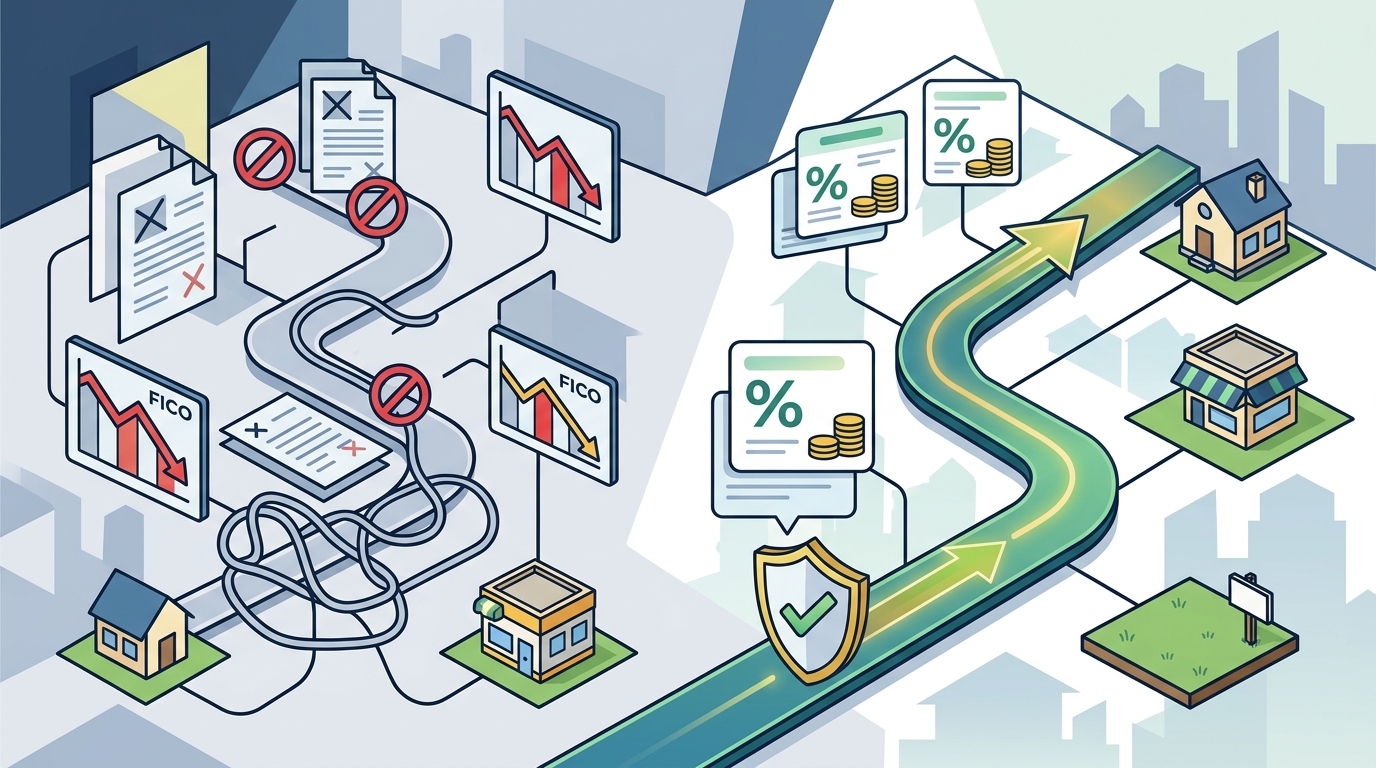

Shopping for a hard money loan usually means handing over your Social Security number to every lender you contact and watching hard inquiries stack up on your credit report. Each inquiry can shave a few points off your FICO score, and the damage compounds fast when you are reaching out to five, ten, or fifteen lenders. The good news: modern loan marketplaces and asset-based underwriting practices let you gather real rate quotes without triggering a single hard pull. This guide walks you through the exact steps, tools, and strategies to compare hard money loan rates while keeping your credit profile intact.

What Is a Hard Money Loan?

A hard money loan is a short-term, asset-based loan secured by the value of a real estate property rather than the borrower's creditworthiness. Unlike conventional mortgages issued by banks, hard money loans are funded by private investors or portfolio lenders and approved primarily on the ratio between the loan amount and the property's market value.

These loans typically carry interest rates between 9.5% and 15%, with terms of 6 to 36 months. They are popular for fix-and-flip projects, bridge financing, and properties too distressed to qualify for bank loans. Because the collateral drives the decision, borrowers with low credit scores or non-traditional income can still access capital.

Why Credit Pulls Matter for Real Estate Investors

Every hard inquiry stays on your credit report for up to two years, according to the Consumer Financial Protection Bureau. When you contact multiple lenders individually and each one runs a hard pull, those inquiries add up. For an investor comparing five or more lenders, the cumulative score drop can push you into a higher rate tier on future conventional financing.

This creates a painful irony: the more diligently you shop for the best rate, the more your credit suffers. That is why platforms that allow rate comparison through soft pulls or no-SSN initial quotes have become essential for savvy borrowers.

Soft Pull vs. Hard Pull: Key Differences

A soft credit pull is an inquiry that does not affect your credit score and is invisible to other lenders. A hard credit pull is a formal inquiry that appears on your report and can lower your score by 5 to 10 points per inquiry. Understanding this distinction is the foundation of credit-smart rate shopping.

When Lenders Use Each Type

Most hard money lenders use property-focused underwriting rather than credit-based approval. Some perform a soft pull as part of due diligence, but it is not a gating factor in the approval decision. Platforms like Lendersa's hard money calculator let you explore rates and terms without providing your SSN at all.

The Marketplace Advantage

A loan marketplace is a platform that broadcasts your deal to multiple lenders simultaneously so they compete for your business. Instead of contacting lenders one by one and triggering separate inquiries, you submit one request and receive competing offers. Lendersa's AI matching engine analyzes your loan scenario and connects you with 3 to 6 best-fit lenders, all without requiring a hard credit pull upfront.

Step-by-Step: Compare Rates Without a Hard Inquiry

Step 1: Package Your Deal First

Before contacting any lender, assemble the key details: property type, location, estimated value, purchase price (if applicable), desired loan amount, and your exit strategy. Hard money underwriting starts with the property, so having these figures ready lets lenders quote you accurately without needing your credit file.

Step 2: Use an AI-Powered Loan Calculator

Enter your scenario into Lendersa's Advanced Calculator, which compares your request against thousands of loan programs from private investors nationwide. The calculator factors in 15 separate variables, far more than the 4 to 7 used by typical mortgage calculators, and delivers results in seconds with no SSN required.

Step 3: Let Lenders Compete

Convert your calculator results into a loan request on the platform. Lendersa's AI instantly broadcasts your deal to matching lenders who then submit competing proposals to your dashboard. You review offers side by side, comparing interest rates, origination points, LTV limits, and closing timelines before choosing which lender to engage formally.

What Drives Hard Money Loan Rates in 2026

Several factors determine the rate a hard money lender will offer you. Loan-to-value ratio is the most influential: lower LTV means less risk for the lender and a lower rate for you. Property type and condition also matter; a stabilized rental in a metro area commands better terms than raw vacant land.

Borrower experience plays a role too. A documented track record of successful flips or rentals signals lower risk, which can translate into rate reductions. Even your exit strategy affects pricing: lenders want to see a clear plan to repay, whether through a sale, refinance, or rental income stabilization.

Current first-position hard money rates generally fall in the 9.5% to 12% range, while second-position loans run 12% to 14%. Origination fees typically add 1 to 5 points.

Hard Money vs. Conventional Loan Comparison

| Factor | Hard Money Loan | Conventional Loan |

|---|---|---|

| Interest Rate | 9.5% – 15% | 6% – 8% |

| Approval Speed | 5 – 15 business days | 30 – 60 days |

| Credit Requirements | Minimal or none; asset-based | 680+ FICO typical |

| LTV Range | 60% – 75% (up to 90%+ for fix-and-flip) | 80% – 97% |

| Loan Term | 6 – 36 months | 15 – 30 years |

| Income Verification | Often not required | Full documentation required |

| Origination Fees | 1 – 5 points | 0.5 – 1 point |

| Credit Pull to Quote | Soft pull or none on marketplace platforms | Hard pull at application |

Key Takeaways

- Hard money lenders primarily underwrite based on property value and LTV, not your credit score.

- Each hard credit inquiry can lower your FICO by 5 to 10 points; multiple lender contacts compound the damage.

- Loan marketplaces let you collect competing offers from a single submission with no hard pull required.

- Current first-position hard money rates in 2026 range from roughly 9.5% to 12%, plus 1 to 5 origination points.

- Packaging your deal details before contacting lenders ensures you receive accurate quotes without unnecessary inquiries.

- Lendersa's AI calculator evaluates 15 factors and matches you with top lenders, all without requiring your SSN.

- Always compare total loan cost, including fees and points, not just the headline interest rate.

Frequently Asked Questions

Can I get a hard money loan with bad credit?

Yes. Hard money lenders focus on the property's equity, not your credit score. Borrowers with scores as low as 450 have successfully secured hard money financing when the deal's LTV and exit strategy were strong. Learn more about hard money loan types on Lendersa.

Do hard money lenders require a credit check?

Many do not. Some perform a soft pull as part of due diligence, but it does not affect your score. Asset-based lenders evaluate the property and your equity position rather than running a formal credit check.

What is the average hard money loan rate in 2026?

First-position hard money loan rates currently range from about 9.5% to 12%. Second-position rates run higher, typically 12% to 14%. Your actual rate depends on LTV, property type, location, and borrower experience.

How fast can a hard money loan close?

Most hard money loans close in 7 to 14 days. Some direct lenders advertise closings in as few as 5 days. By contrast, conventional financing typically takes 30 to 60 days.

What is a loan marketplace?

A loan marketplace is a platform that connects borrowers with multiple lenders at once, allowing them to compare and contrast loan offers. Lendersa is a loan marketplace where lenders compete for your deal across residential, commercial, and vacant land properties.

Do I need to provide my SSN to compare rates?

Not on Lendersa. You can use the Advanced Calculator and submit a loan request without providing your Social Security number. A formal SSN is only needed later when you choose a lender and move to a full application.

What fees should I watch for beyond the interest rate?

Look out for origination points (1% to 5% of the loan), appraisal fees, document preparation fees, and any prepayment penalties. Always request a written quote that details the nominal rate, all fees, and the true APR before committing.

Is a hard money loan right for a long-term rental hold?

Generally, no. Hard money loans are designed for short-term strategies like fix-and-flip or bridge financing. For long-term holds, explore Non-QM or DSCR loan programs that offer lower rates and longer terms.

Get Your Rate Quote Today

Stop letting hard credit pulls chip away at your score every time you shop for financing. Use Lendersa's free Advanced Calculator to compare hard money loan programs from thousands of lenders in seconds, with no SSN required. Enter your property details, review your LoanScore, and let competing lenders come to you with their best offers. Start now and keep your credit intact while you find the best deal.